4: The Adjustment Process Business LibreTexts

An accounting period breaks down company financial information into specific time spans, and can cover a month, a quarter, a half-year, or a full year. Public companies governed by GAAP are required to present quarterly (three-month) accounting period financial statements called 10-Qs. However, most public and private companies keep monthly, quarterly, and yearly (annual) period information. This is useful to users needing up-to-date financial data to make decisions about company investment and growth. When the company keeps yearly information, the year could be based on a fiscal or calendar year.

Guidelines Supporting Adjusting Entries

Interest can be earned from bank account holdings, notes receivable, and some accounts receivables (depending on the contract). Interest had been accumulating during the period and needs to be adjusted to reflect interest earned at the end of the period. Note that this interest has not been paid at the end of the period, only earned. This aligns with the revenue recognition principle to recognize revenue when earned, even if cash has yet to be collected.

( . Adjusting entries for accruing uncollected revenue:

Even though not all of the $48,000 was probably collected on the same day, we record it as if it was for simplicity’s sake. Supplies increases (debit) for $400, and Cash decreases (credit) for $400. When the company recognizes the supplies usage, the following adjusting entry occurs. The unadjusted trial balance may have incorrect balances in some accounts.

Adjusting Entries

Using the tableprovided, for each entry write down the income statement accountand balance sheet account used in the adjusting entry in theappropriate column. Accruals are types of adjusting entries thataccumulate during a period, where amounts were previouslyunrecorded. The two specific types of adjustments are accruedrevenues and accrued expenses. Unearned revenue represents a customer’s advanced payment for a product or service that has yet to be provided by the company. Since the company has not yet provided the product or service, it cannot recognize the customer’s payment as revenue. At the end of a period, the company will review the account to see if any of the unearned revenue has been earned.

- When the company provides the printing services for the customer, the customer will not send the company a reminder that revenue has now been earned.

- Perhaps the single most important element of accounting judgment is to develop an appreciation for the correct measurement of revenues and expenses.

- Did we continue to follow the rules of adjusting entries in these two examples?

However, one important fact that we needto address now is that the book value of an asset is notnecessarily the price at which the asset would sell. The same is true about just about any asset youcan name, except, perhaps, cash itself. The book value of an asset is not necessarily the price at which the asset would sell. If you’re short on time, you can cook a frozen roast in a slow cooker, but you’ll need to adjust the cooking time.

Simply season the roast, place it in the slow cooker, and let it cook while you attend to other tasks. This method is perfect for busy individuals who want to come home to a ready-to-eat meal. Place the lid on the slow cooker and cook the roast on low for 8-10 hours or on high for 4-6 hours.

It is the end of the first month and thecompany needs to record an adjusting entry to recognize theinsurance used during the month. The following entries show theinitial payment for the policy and the subsequent adjusting entryfor one month of insurance usage. He does the accountinghimself and uses an accrual basis for accounting. At the end of hisfirst month, he reviews his records and realizes there are a fewinaccuracies on this unadjusted trial balance. The accounting cycle is a comprehensive accounting process that begins and ends in an accounting period. It involves eight steps that ensure the proper recording and reporting of financial transactions.

The financial statements must remain up to date, so an adjusting entry is needed during the month to show salaries previously unrecorded and unpaid at the end of the month. The accounting in between stimulus payments retail sales decline cycle is started and completed within an accounting period, the time in which financial statements are prepared. However, the most common type of accounting period is the annual period.

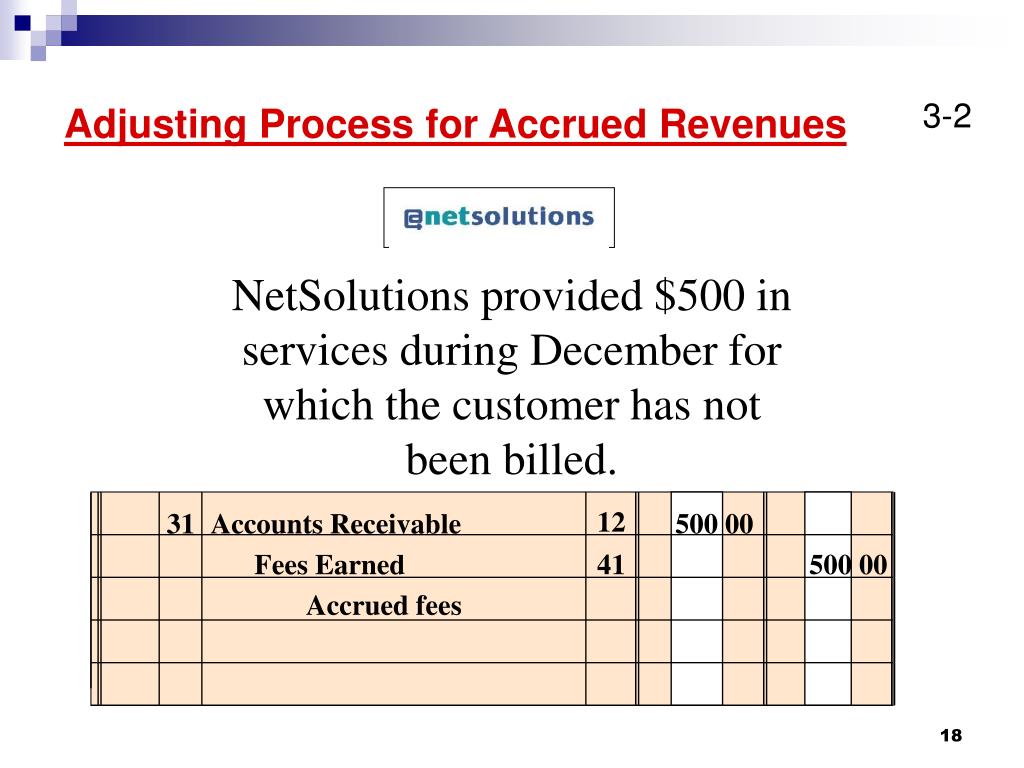

Accounts Receivable increases (debit) for $1,500 because thecustomer has not yet paid for services completed. Service Revenueincreases (credit) for $1,500 because service revenue was earnedbut had been previously unrecorded. For example, let’s say a company pays $2,000 for equipment thatis supposed to last four years. The company wants to depreciate theasset over those four years equally. This means the asset will lose$500 in value each year ($2,000/four years).

This allocation of cost is recorded overthe useful life of the asset, or the time periodover which an asset cost is allocated. The allocated cost up tothat point is recorded in Accumulated Depreciation, a contra assetaccount. A contra account is an account pairedwith another account type, has an opposite normal balance to thepaired account, and reduces the balance in the paired account atthe end of a period. Adjusting entries requires updates to specific account types atthe end of the period.